AI is not something people aren’t aware of. The biggest buzzword of 2025 and the most advanced technology of the 21st century are changing how businesses used to work. The fintech industry is also undergoing significant changes due to artificial intelligence. The importance of AI in digital payments can be understood from the fact that the global AI in finance and payment market is going to reach $190 billion in 2030 from $38 billion in 2024.

AI tools empower fintech firms by improving their operations, preventing fraud, and providing a delightful customer experience. Moreover, artificial intelligence in digital payments helps fintech firms enhance security by detecting anomalies in real time. AI is used to make chatbots and agents that can provide instant answers to the questions of customers. Read this blog to learn about AI in digital payments, its use cases, challenges, and key AI tools and technologies banks can use to create AI tools.

What’s AI in payments?

Artificial intelligence refers to the use of AI tools to streamline the operations of the fintech industry, such as financial transactions and payment processes. Different from traditional methods, which used to work on predefined rules and frameworks, AI continuously learns from the data it gets. This helps it automate routine tasks, detect fraud, and provide a personalized experience to customers. Apart from this, AI also enhances security and improves efficiency and productivity.

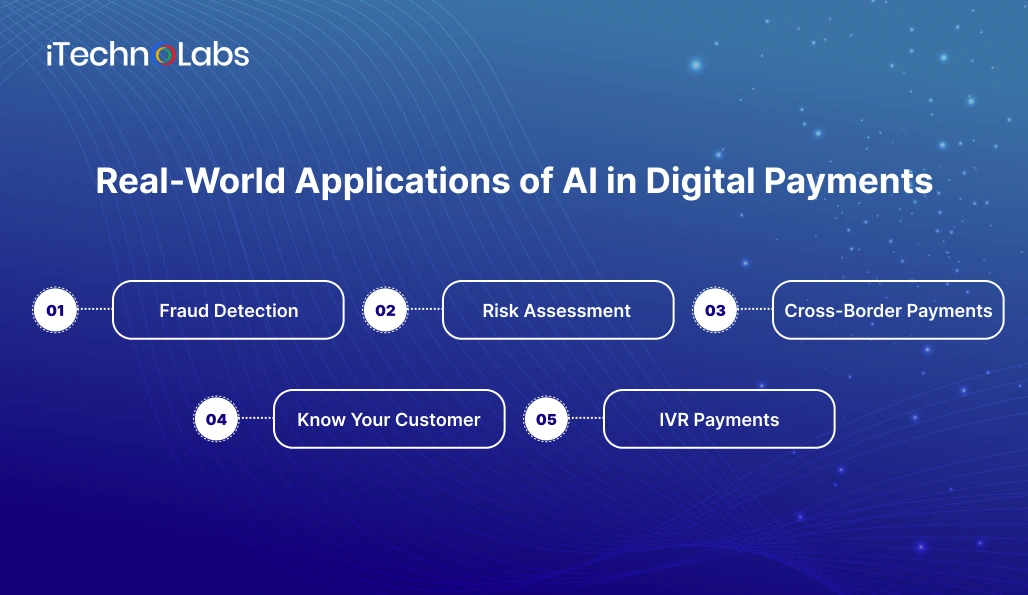

Real-World Applications of AI in Digital Payments

Many companies now use AI to make sure your payments go through smoothly and safely. Whether you’re buying a game, paying bills, or sending money to a friend, AI works quietly in the background to keep things running well. In the next section, let’s explore some real-world examples of how AI is making digital payments easier and more secure for everyone.

1. Fraud Detection

Artificial intelligence tools can analyze huge amounts of data in seconds and can monitor live transactions as they take place. This allows it to detect any kind of anomalies in real-time and inform the concerned team to take necessary action.

Example – PayPal

Being one of the world’s biggest fintech companies, PayPal sees billions of transactions take place every day. That opens room for cyber attacks. But PayPal has in place an AI-powered trick-spotting tech that helps it detect fraud. Here’s how it works:

- Transaction velocity: The AI tool monitors live transactions, and if too many transactions take place in the blink of an eye, it shows red flags.

- IP addresses: The AI tool keeps an eye on where the transactions are coming from. Is someone popping up from uk right after using a New Zealand login? That sounds scammy.

2. Risk Assessment

Risk assessment in payments means using AI to find and measure potential dangers, like fraud or someone not paying a loan back. AI looks at lots of data like credit history, transaction frequency, and social signals to spot risky behavior. It scores each deal or person to decide how risky they are. AI learns from past fraud cases and can even discover new tricky schemes without examples. A real example is Stripe, which uses AI to check if a business is risky before letting it join its platform. This helps Stripe reduce false declines and recover more money.

3. Cross-Border Payments

Sending money overseas is still a tricky thing. There are so many rules one has to take care of. Moreover, there are various charges, and still, the process takes 3-5 days at a minimum. This is a challenge for a firm or individual who constantly sends or receives money across borders.

AI is transforming this too by analyzing the market in real-time. It predicts the future pricing movement and foreign exchange currency rate, preventing people from losing money. Additionally, AI in payments tells the best method to send or receive money.

Example – Wise (Transfer Wise)

Wise has changed how people used to send and receive cross-border payments. The AI programs monitor and guess where popular currency pairs like USD to EUR are heading. Wise checks all the boxes and compares payment partners across the globe to find the route that will cost you the least.

4. Know Your Customer

Know Your Customer, or KYC, is a way that banks and companies make sure people are really who they say they are. This helps stop bad guys from using fake identities to steal money or do illegal things. When someone signs up, they take pictures of their ID, like a passport or driver’s license, and a selfie. Then, special computers use AI to check if the ID matches the person’s face and if all the info is correct.

A good example is Revolut, a popular company that offers banking services. When new users sign up, they upload their ID and take a selfie. The AI then scans the ID and matches it to the selfie. It also checks if the person is on any bad lists to stop fraud. This helps Revolut keep its system safe and stop fake accounts from being created. Thanks to this, they reduced money lost to fraud by 30%.

5. IVR Payments

IVR payments refer to the payments people make over the phone without talking with a real person. They just have to hit a number and follow the robot’s voice to make the payment. By just ringing your number and feeding in card details, your payment is done. Many companies use IVR to handle a large number of payments.

Example – American Express

American Express uses AI very well in IVR payments. It has merged AI with IVR, which lets people pay by just talking through their cards. Let’s say someone with an American Express card rings them up. Now the AI will pop up and will ask want to use the card number ending with 8473 or how much you want to pay. This lets people pay quickly and seamlessly.

Also, read: AI Chatbot in Healthcare: Transforming Patient Care with Medical AI Chatbots

AI Tools and Technologies for the Payment Industry

There is a wide range of AI technologies and tools used by fintech companies in their operations. The AI tool and technology for every company vary depending on their needs and budget. The following are some of the popular AI tech stacks used in the fintech industry:

1. Machine learning algorithm

Machine learning algorithms make payment setup smarter on their own without telling them what to do. Here’s how machine learning works:

- Fraud detection: Machine learning models help to detect weird patterns in transactions. They detect where you are, the device you are using, and what you are going to buy to find if something is off. If it gets any dodgy dealings, it puts a risk number on it to show that it needs a closer look.

- Predictive analytics: The advanced tool makes businesses aware of the activities of customers such as if they are going to splash their cash, or if they are going to buy something next month. This helps firms handle customers better and keep enough staff to manage them.

2. Natural language processing

Natural language processing, or NLP, is the advanced software that tells computers what to say. Here are its uses:

- Voice-based transactions: Alexa and Siri can handle cash transactions by just listening to what you say because of natural language processing. With NLP, you can take care of your bills with just your voice.

- Chatbots: The NLP-powered chatbots are available round the clock to answer any questions of customers regarding foreign exchange rates, best FD returns, investment plans, and more. This ultimately cuts down costs for fintech firms and provides a quick service to the customers.

3. Generative AI

Generative AI in payments continuously learns from patterns and adapts accordingly. Below are some of its use cases:

- Content creation: By learning about the spending habits of people, generative AI can create customized emails or promotional content.

- Personalization: Generative AI continuously monitors how much a person spends in a month and on what things. This helps it to suggest personalized recommendations.

4. Blockchain

Blockchain is like a digital notebook that everyone can see but no one can erase or change without permission. In the fintech world, it helps people send money safely and quickly without needing banks as middlemen. This means less waiting and fewer fees. It also helps stop cheating because every transaction is recorded clearly. Smart contracts are special computer programs on blockchain that automatically do things like pay someone when a job is done. Overall, blockchain makes money transfers, loans, and buying things easier and safer for everyone, anywhere in the world.

5. Computer vision

Computer vision comes into the picture when it’s about visual information. It ensures all rules are followed while payments take place. Here are its uses:

- Identity verification: The system checks the ID or passport when a person makes a new account or makes a big payment.

- Document scanning: Many money exchange platforms and shops use AI in payment to scan documents without mistakes.

6. Quantum computing

Quantum computing helps the fintech industry by making very fast calculations and finding patterns in large sets of financial data. It uses special ‘qubits’ that can do many things at once, so banks and businesses can make better and faster decisions. This helps with managing investments, finding risks, and stopping fraud. Quantum computers can also make transactions quicker and safer with advanced security methods. Overall, quantum computing makes money systems smarter and more secure, helping banks and customers do better with their money every day. This is like having a super-smart helper for big money problems in fintech.

7. Decentralized finance

In decentralized finance, transactions are transparent, secure, and automated using smart contracts. This system also lowers fees and makes financial activities more accessible, especially to people who don’t have banks nearby. DeFi is changing how money works by giving people more control and reducing costs in finance.

Challenges in AI for Digital Payments

AI is changing how we pay for things online, but it’s not always easy. There are problems that can slow it down or make it less safe. Sometimes AI makes mistakes, or hackers try to trick it. Other times, the system can be too slow or hard to understand. In this section, we’ll look at the main challenges AI faces in digital payments and why fixing them is so important for keeping money safe.

1. Data privacy

One of the biggest challenges of implementing AI in digital payments is data security. People may get worried if a machine is handling all their data, like personal and bank details. Further, not complying with rules such as GDPR or CCPA is going to cost you a lot.

Solution – Use the advanced encryption methods and keep the data anonymous. Stick to a privacy-first idea and only adopt those tools that follow data protection rules. Make sure the data methods are clear, and you check systems regularly to build customer trust.

2. Need for human oversight

AI can automate many tasks, but it still hasn’t reached the level where it can do everything without manual guidance. The artificial intelligence in digital payments is still learning and can make mistakes at times you are not expecting.

Solution – Try a hybrid solution where AI will do the easy stuff, and you can take care of the big decisions that can affect the company on a large scale. Always monitor what’s going on and give feedback to AI so it can improve.

3. Ethical issues

Another major risk while implementing AI in payments is the ethical considerations. It must be able to deal with tricky moral issues. It needs to make sure that everyone has an equal chance to use the financial tool and not do anything scammy. Chances are, AI might leave people who don’t use these services or give preference to those who make more money than others.

Solution – Create AI tools that put people first and involve people while building them. Do ethics checks regularly. In this way, the AI will match what people think instead of causing trouble.

4. Fraud tricks

On one side, AI is getting smarter, but on the other side, the bad buys are also learning new tricks. They are coming with fake identities using deepfakes. This leads to a constant fight between the two.

Solution – Implement super-advanced AI solutions that can detect any anomalies or suspicious patterns in real-time, preventing fraud. Collaborate with IT teams and find out the best ways to deal with cyber attacks.

5. Implementation cost

AI is not merely a tool for which you can just pay a monthly subscription fee, but a framework that can cost a fortune for companies. Large companies might be able to pay for this, but small companies are only going to struggle.

Solution – Firstly, start small, and as your business grows, you can use better and expensive AI models. You can partner with other companies to share costs or explore open-source tech to keep expenses under budget.

6. AI bias and fairness

AI in the payments industry learns from the data it gets. If the data is inaccurate, the AI will generate irrelevant results. This will lead to severe consequences, such as who will get a loan approved and whose loan will be rejected. It’s not good as it will hit some people harder than others.

Solution – Use a variety of data sets to train AI models and make sure you are checking them regularly using tests created to measure fairness. Go for AI tools that explain their results so you can easily fix the issue.

7. Hiccups with structured data

In the fintech industry, structured data means organizing information in a clear, neat way so computers and AI can easily understand and use it. However, hiccups happen when this data is messy or mixed up, making it hard for AI to do its job well. This can lead to mistakes in things like spotting fraud or managing customer accounts.

Another problem is that fintech companies often have data stored in different places or formats, which confuses AI systems. These challenges slow down AI’s ability to help with tasks and can cause trust issues with customers because the results might be wrong or unclear.

Suggested article: Agentic AI in Banking: Use Cases That Drive Growth & Innovation

Conclusion

Gone is the time when banks had to do everything on their own. Now they can integrate AI systems into their processes to save time and cost, and focus on making strategies for the future. The benefits of using AI in digital payments can’t be neglected. Some of the major advantages of artificial intelligence in fintech are fraud detection, improved efficiency, enhanced security, improved customer experience, better risk management, and more. Using technologies like machine learning, natural language processing, computer vision, data analysis, blockchain, and many more, banks can create customized AI tools according to their requirements and budget.

Along with the benefits come multiple challenges while implementing AI in payments, such as data security, constant human intervention, ethical issues, high implementation cost, and bias. But you don’t need to deal with any of these, as you can partner with iTechnolabs, a renowned AI development company. With its 9+ years of experience and 230+ AI experts, iTechnolabs can create the best AI tools for your daily operations. Visit the website now and ride the AI wave for the betterment of your business.

FAQs

1. How is AI transforming payments?

AI is revolutionizing the fintech industry by helping banks automate routine tasks, provide personalized services to customers, and improve efficiency. Further, it helps to enhance the security, increase revenue, and more.

2. What is the role of AI in fintech and digital payment?

The role of AI in fintech and digital payment is to safeguard customers from cyberattacks, improve the productivity of banks’ employees, and provide personalized financial advice.

3. How does AI help banks and money stuff?

AI helps banks by making things faster and safer. It can help find fake transactions, give customers advice, and make loans quicker. AI can also talk to people through chatbots, which are like robot helpers that answer questions anytime. This makes banking easier for everyone and keeps money safe.

4. Can AI stop bad people from cheating?

Yes, AI can find when someone is trying to cheat or steal money. It looks at data and watches for odd activities that don’t seem normal. If AI sees something suspicious, it alerts the bank so they can stop the bad stuff and keep your money safe.

5. Will AI change how banks work in the future?

Yes, AI will keep changing banks by making their work faster, smarter, and more fun for customers. It will help with new ideas and better ways to help people. Banks are studying how to use AI to make banking better and safer for everyone.